Certainly many young crypto traders heard about foreign exchange arbitrage trading. They were even going to make the transaction, on the basis of a particular technique of carrying out of such operations.

Arbinox specialists offer to understand the basic concepts of crypto currency arbitration. They propose to consider several popular schemes for its implementation. It is proposed to assess the possible risks of such operations.

“All wealth is based upon systems”

Dan Kennedy

So let’s start with the definition. Arbitrage (from the French. “arbitrage” is a fair solution) is a series of logically related transactions. They aim to profit from the difference in prices of the same or related assets.

There are two definitions:

Spatial arbitration

When talking about market arbitration in a narrow sense, first of all one should bear in mind spatial arbitration.

The simplest algorithm for such operations is as follows: let’s say, on two different exchanges quotes are markedly different. Accordingly, buying an asset on the first exchange at a lower quotation and selling it on the second at a more profitable, the trader will receive his profit.

At its core, exchange arbitrage is the exploitation of the inefficiency of quoting an individual broker/exchange or the financial system as a whole. At the same time, the less centralized the financial system, the worse the inter-exchange communication — the more opportunities for the arbitrage. That is why arbitrage operations with cryptocurrencies are currently extremely relevant.

Well, let’s get down to specifics. We will analyze several arbitration schemes. And we will analyze their features.

Back to our simple example with the difference of quotations. On the stock exchange No. 1 quote of the BTC/USD = $5 000, at the exchange No. 2 — $5 500. Buy on the stock exchange №1 (paying attention to the Ask-orders in the “stock glass”). Then we transfer to the exchange number 2 and sell there. As a result, we get $500 (10%) “dirty” profit, which should be called “inter-exchange spread”.

It would seem that everything is quite simple. However, $500 in our example represents a “dirty” profit. “Clean” net profit, we, in fact, get several less (and sometimes much less).

Why is this happening? The answer is simple: because of the various commissions:

Most arbitrators, of course, take into account all these transaction costs. They work with an inter-exchange spread of 1-2% and above. They are also working on various schemes to reduce transaction fees.

This is perhaps one of the most important points that should be taken into account before conducting arbitration operations. Often, a large inter-exchange spread is observed among low-liquid altcoins, trade volumes of which are quite small. In such cases, “crank” large operations become very problematic.

Professional arbitrators work mainly on large volumes. This approach allows to minimize transaction costs.

Also, do not lose sight of the fact that a lot of players are trying to get the arbitration benefit at once. This means that with a large difference in prices at different sites, any volume will be selected quickly enough. As a result, the arbitrage trader loses potential profit due to the rapid reduction of the inter-exchange spread.

All actions for spatial arbitration must be performed practically (and even better — literally) at the same time. Otherwise, the quotes will change and the inter-exchange spread will be smoothed. There is a high probability that the operation will become unprofitable.

In the example we are considering, this risk mainly occurs at the stage of transfer of funds. From one exchange to another and from an external wallet to the exchange. The delay may arise from the exchange itself. For example, in connection with technical works, the wallet of a crypto asset may not work either for replenishment or for withdrawal.

Also, the risk increases with a strong blockchain load of a particular cryptocurrency. This results in slow transaction processing. As for the number one cryptocurrency, even despite the recent decrease in the average size of fees and some increase in the speed of transaction confirmation, the transfer of funds from the wallet to the wallet will still take some time. During this time, the market situation may change greatly. For this reason, the bitcoin network is not very suitable for arbitration operations that require fast transactions.

According to the degree of automation of arbitration operations, there are several categories of traders:

The main problem of inter-exchange arbitration under the first scheme is the need for rapid transfer of funds from exchange No. 1 to exchange No. 2. Let’s try to exclude this component. The second scheme will be effective in investing assets in the medium/long term, especially at the time of pump.

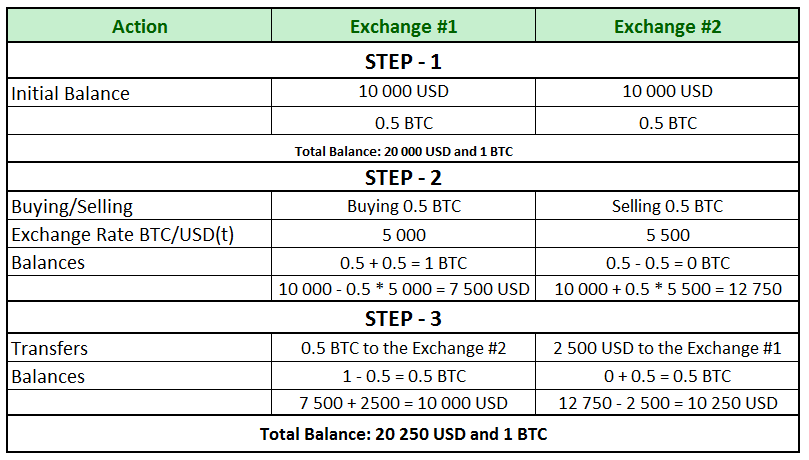

Suppose that we have 1 Bitcoin BTC and 20 000 USD(T), we hold two exchanges 50/50 for risk diversification (see table — STEP 1).

When an inter-exchange spread appears, we buy BTC (at the expense of USD(T) in our wallet) on the first exchange and sell them completely on the second (see STEP 2), after which we make two transfers from the exchange to the exchange to restore the balance (STEP 3).

In this example, transaction costs are not taken into account, however, it is certainly necessary to remember them. So, in our case, the “dirty” arbitrage profit was 0.05 BTC.

Now for the cons of this scheme:

The ability of inside arbitration occurs when the inefficiency of the quotation within the same site. Suppose we have at our disposal 10 000 USDT, and on the exchange there was the following situation with quotes:

In this situation, the “dirty” arbitration profit can be 357 USDT.

The chain of intra-exchange arbitrage operations may not be limited to three assets, but may be longer and comprise, for example, four assets or even more.

The disadvantage of this scheme is the increased risk of rapid changes in quotations. For greater efficiency need full automation of search and execution of applications.

It is also worth noting that some exchanges introduce an additional delay for processing market orders using the API, which can significantly affect the final financial result.

Conclusion

The above three schemes of arbitrage operations with crypto assets are the simplest and popular among traders. To try yourself in arbitration or not – you decide. However, I would like to repeat that at the moment the relevance of such speculation leaves no doubt, since the crypto market has not been finally formed and is in constant development.

However, the benefit can also be derived during periods of impulsive or strong trend movement of the asset price, especially if it is possible to predict it in advance.

This scheme is largely dependent on significant events and impulsive movements in the market, as well as the ability to predict the trend movement.

When trading in the foreign exchange market, such events can be, for example, the publication of macroeconomic data (NFP every first Friday of a new month or the interest rate of the US Federal reserve). The concept of news trading is still poorly developed in the crypto market, but trading on a similar principle is still possible.

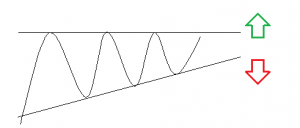

It should also be noted that such popular graphical figures of technical analysis as a triangle, when broken, are equally likely to cause the movement of quotations up or down. In this case, it is likely to be pulsed:

The popular figure of technical analysis “Triangle”. Breaking through one of its sides up or down is often accompanied by a powerful movement of the asset price.

For this type of arbitrage trading, it is necessary to use two crypto-currency exchanges, where the possibility of margin trading (for example, Bitfinex and Poloniex) is presented, since it will be necessary to open positions for a decrease.

On one exchange, we open a position for an increase, on the other — for a decrease before the moment of penetration of the figure. Positions must be in the aggregate market neutral. In other words, the collateral, margin and opening quotes must be identical.

Next, there are options for closing the position:

— without placing pending orders (closing a losing position when the percentage values of Margin Call/Stop Out Are reached);

— setting of pending orders (Stop Loss/Take Profit); closing at the specified quotes.

Closing one of the transactions (partially or completely) with a loss, we get profit from the second position. The difference between them will be the trader’s arbitrage profit.

This method of arbitration is not recommended for beginners, because it is necessary to correctly and carefully choose the strategy of money management, as well as the size of the position in relation to the size of the market movement. Do not forget that margin security is provided on credit, for which you will need to pay interest.

The main disadvantage of this scheme is the trading risk. It includes possible slippage of order processing, knocking out one or both positions on the hyper volatile market by Stop Loss, etc. Also, not all assets can be traded with margin collateral, their number is limited.

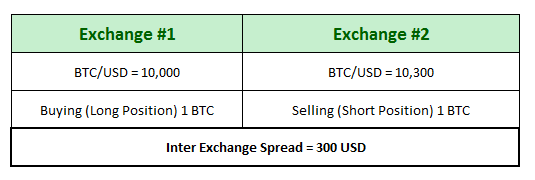

This arbitrage trading method will also require margin trading, implying the ability to trade on the downside. Let’s consider the scheme on the example of BTC/USD(T) currency pair.

Suppose one exchange quotes BTC/USD = $10 000, and the other — $10 300. On the first exchange, we open a position for an increase, on the second — for a decrease with the same volume:

As you can see, the aggregate position will again be market neutral. In other words, if the exchange rate of BTC/USD changes, the profit of one position will be equal to the loss on the other (provided the same amount and percentage of borrowed coins for margin security).

What can a trader earn here? The fact is that the spread is not a constant value and in this case, the change in quotations plays into the hands of the arbitrage. After fixing the spread of $300, you should wait until it changes to the desired value (for example, $150), and then close all positions.

Consider the scheme in more detail:

Overall financial result: (10 500 — 10 000) + (10 300 — 10 650) = 150$

Disadvantages of this scheme:

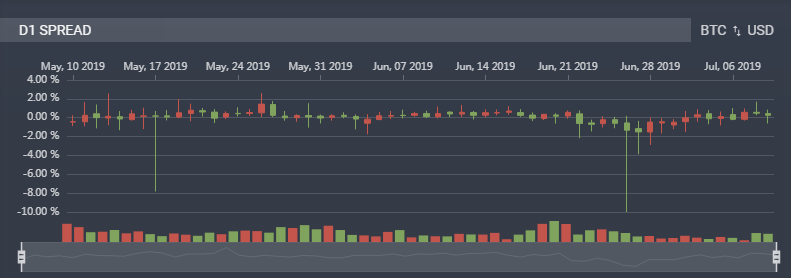

Arbinox Arbitrage Trading Platform provides the best performed Automated Arbitrage Trading Platform based on spread arbitration principle.

The Arbinox system as an analysis proposes to consider the cross-exchange spread as a percentage of divergence. An example of how the spread changes on the daily chart:

Arbitrage spot futures involves on the one hand the purchase of an asset, and on the other — the sale of futures on the same asset.

Often, the futures prices of assets are just above their spot price, and this can be earned. However, for this type of arbitrage, the futures must be deliverable. Unfortunately, at the moment futures on the CME and CBOE bitcoin exchanges are settlement. Therefore, this type of arbitration is not yet available, but everything can change over time.

However, it is already possible to trade calendar spreads between two futures contracts. Let’s assume that the following situation appeared on the market (not because of the difference in the quotes update as in the picture, but in real time):

As you can see from the table, we can buy the March futures and sell the February futures by fixing the calendar spread between them.

Within the meaning and logic of trade, this operation is fully consistent with the previous arbitration scheme. Next, you need to wait for the calendar spread to narrow, and then close the positions. Or you can wait for the expiration of the nearest contract, and then the closure is automatic.

Recently, for Russian traders also opened access to trade futures on bitcoin, but do not forget about the additional Commission (about $20-30).

With the further development of derivative financial instruments (for example, options) on the basis of bitcoin, new opportunities for arbitration operations will appear. At the moment, the opportunity to trade traditional (or, as they say, “vanilla”) options is only on the LedgerX exchange. However, it is expected that the options will begin to appear en masse and actively in the summer of 2019.

In this article we have analyzed several arbitration schemes, both relatively simple and more complex. In fact, there are many more arbitration schemes. For example, pair arbitrage trading, which allows you to earn income by changing the correlation of the two assets, was not considered.

Arbitrage transactions are certainly of interest, especially in the emerging cryptocurrency market. They allow you to get a small income with relatively small risks due to the inefficiency of quoting on different liquidity trading platforms.

To reap significant benefits, you will need a large Deposit, a deep understanding of the market and, preferably, programming skills to create and maintain an arbitration bot.

It should be understood that, despite the wide opportunities for such earnings, the young crypto market is characterized by increased risks.

Jeremy Stone Cryptocurrency Read 7min

Jeremy Stone Investments Read 11min

Jeremy Stone Cryptocurrency Read 8min

Jeremy Stone Cryptocurrency Read 5min

Musqogees Tech Limited 41, Propylaion street RITA COURT 50 4th Floor, Off.401 1048 Nicosia, Cyprus

+357 95 910654

info@musqogee.com